Retirement Planning

7 MIN ARTICLE

Retirement has changed. You may have noticed firsthand with retirees you work with, but research from Capital Group confirms it. No longer a time for slowing down or just sitting around, today’s retirees describe being in the midst of a dynamic modern midlife: a time of reinvention, renewed vitality and deep introspection. They see the future as unwritten and full of opportunity.

This retirement evolution presents a great opportunity for financial professionals to differentiate themselves, add value and support the goals of their clients. But it may take a bigger-picture view and willingness to delve into new areas of planning.

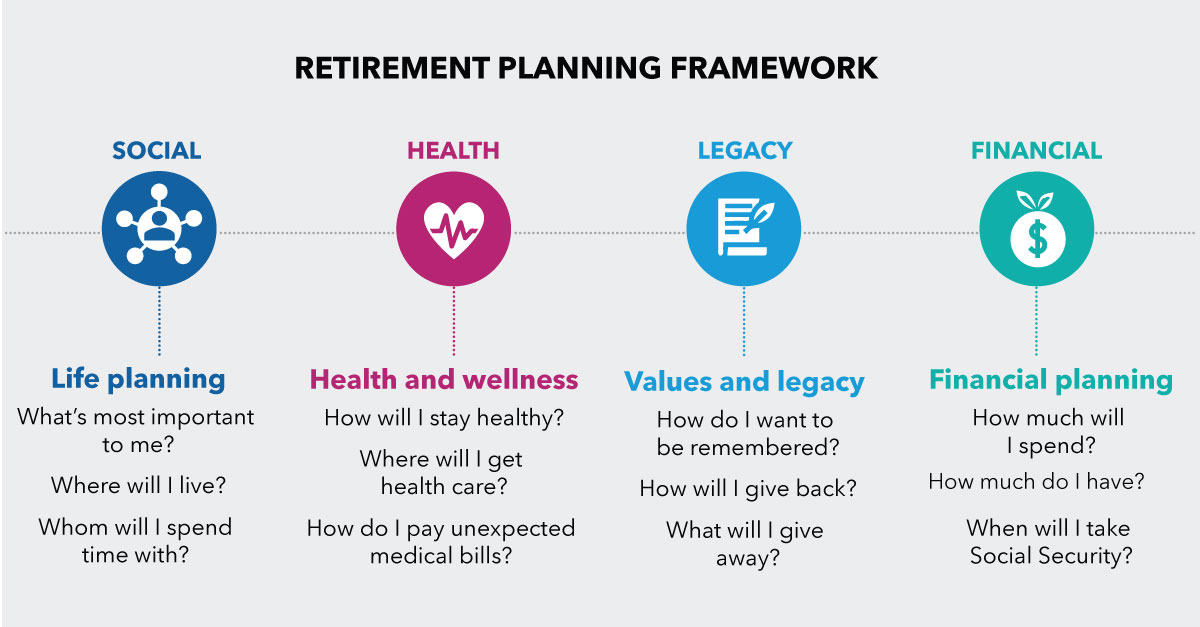

Our retirement planning workbook can help. Based on our latest research and feedback we at Capital Group receive from the thousands of advisors we work with each year, our investor-facing workbook, My Best Retirement can be used to start the conversation with pre-retirees and help you gather important information. It’s based on a framework containing four crucial aspects of planning:

Along with being a planning tool for existing clients, the workbook can be used as an educational tool for prospects. Here’s an overview of the workbook and how to walk through it with investors.

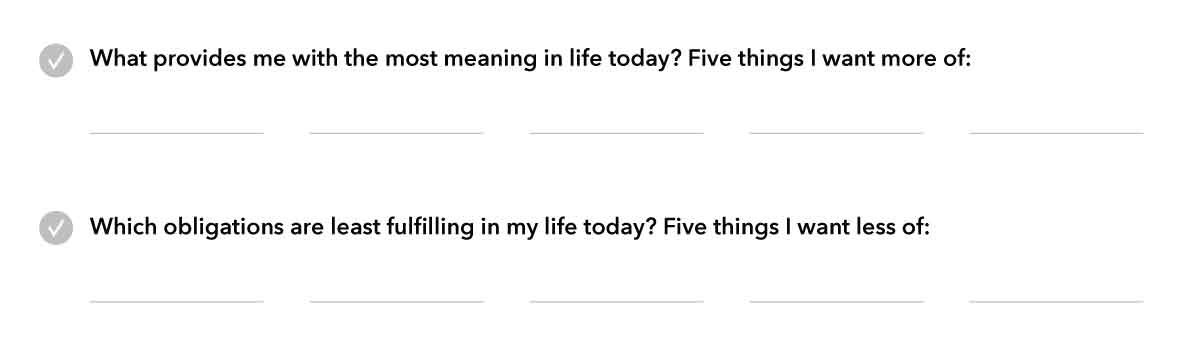

The only rule: Don’t be afraid to think big and to take some time with this work. Encourage a full, rich discussion rather than simply checking boxes. In fact, the workbook begins with some thought-provoking questions. What do you want more and less of in your life?

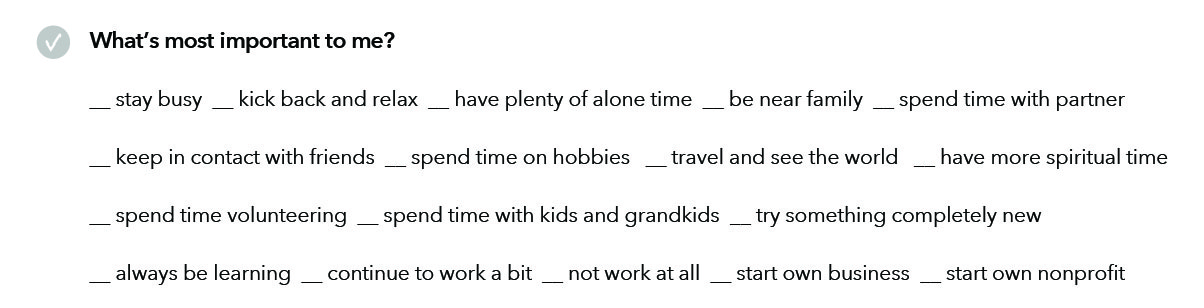

1. Life planning

Start with the area that often gets planned for the least: daily life. It’s easy to think that everything will fall into place when we don’t have to get up for work each day. But adapting to unstructured time can be a challenge. For those people who derive a good amount of their personal fulfillment from work, or who spend a lot of nonworking hours socializing with co-workers, retirement may feel like an abrupt change of pace.

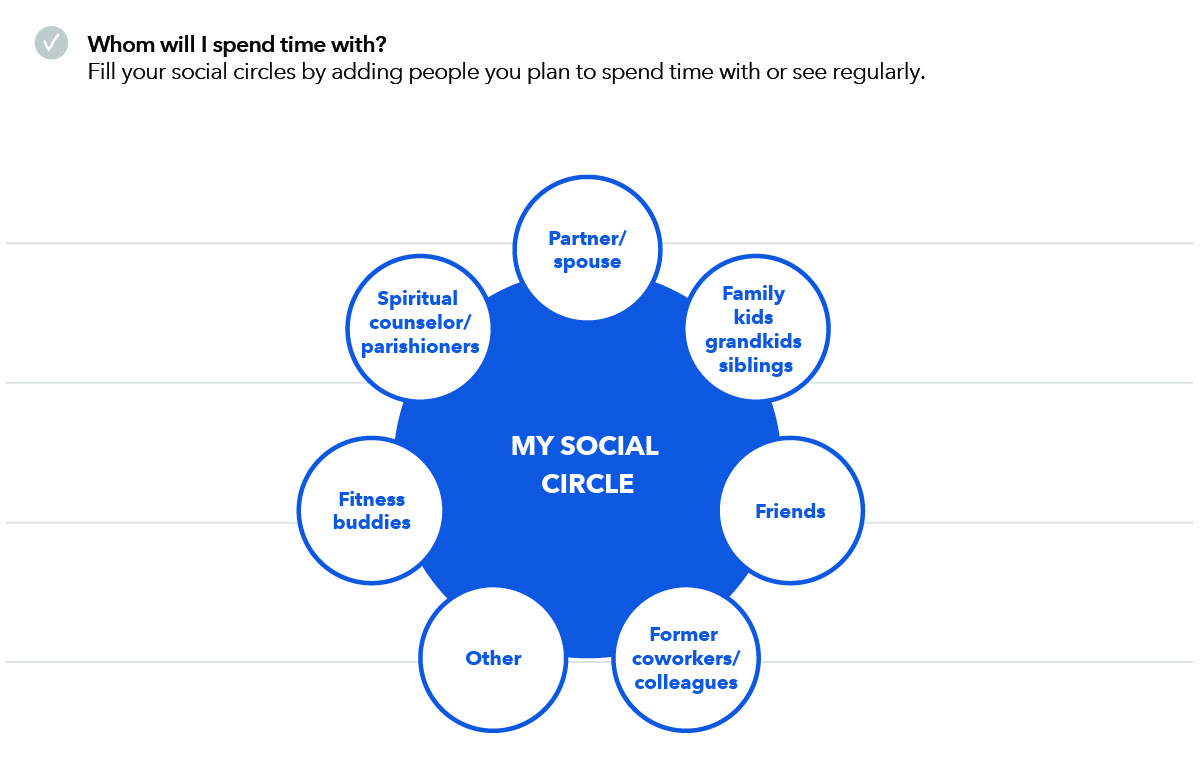

To help investors prepare for it, get them thinking specifically about three key questions: What do they want to do, where do they want to live, and whom will they spend time with?

Source: Capital Group

Another useful tool is a simple blank calendar. What does a typical year look like in retirement? What are the big-picture plans? And then, getting even more specific, what does a typical day look like? Many retirees in our survey set up rules or routines to keep things lively – and attempted to keep busy calendars full of social events and activities.

By understanding where individuals plan to focus their time and where there are gaps, you can help shore up the retiree’s social and professional circles of support. You don’t have to be an expert in any one area, but you can have a point of view — and a list of names ready to take referrals. Think of yourself as a retirement concierge, someone with connections that extend beyond traditional centers of influence. This may include real estate advisors, mortgage brokers and movers, personal trainers or athletic pros, spiritual advisors and community groups, and more.

You can also become an expert in thinking like a retiree, by reading the latest books, listening to podcasts, or staying on top of resources that are designed for the modern midlife demographic. For example, the Retirement Wisdom podcast focuses on the changing nature of retirement and the non-financial aspects involved. The Retirement Manifesto blog and book, “Keys to a Successful Retirement,” by Fritz Gilbert, focus on staying happy, active and productive in your retirement years. And resources such as Encore.org and Roadscholar.org cater to modern midlifers looking for purpose and learning. There are many such resources available, and relatively easy to find.

2. Health and wellness planning

Even a small amount of information about your clients’ general health status can provide insight into longevity and Social Security considerations, along with other implications for the financial plan. But if you don’t feel comfortable asking about personal health, helping clients consider general health issues and plan for health care costs can be a valuable service offering.

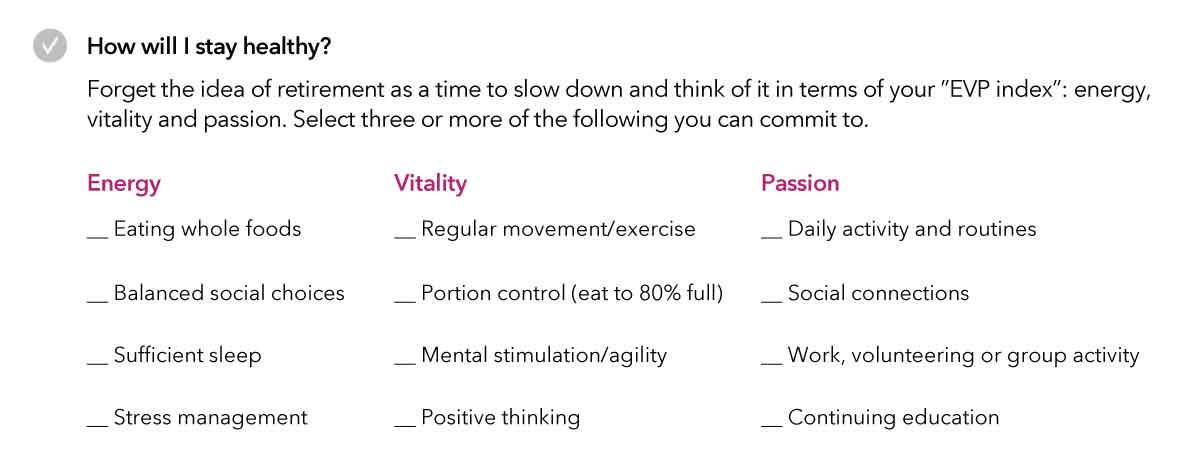

One positive finding in our survey is this generation of retirees may be more energetic, active and engaged. Frank, a 66-year-old retiree, put it best: “Biologically and physically, I’m doing things other people can’t do. I run marathons and cycle for long distances. This fills my EVP index – energy, vitality and passion.”

Our checklist expands on this idea, offering examples of healthy habits that might be included in an “EVP index.” You can review them with clients to see which are most appealing, or which might be a struggle. Aim for a commitment to at least three.

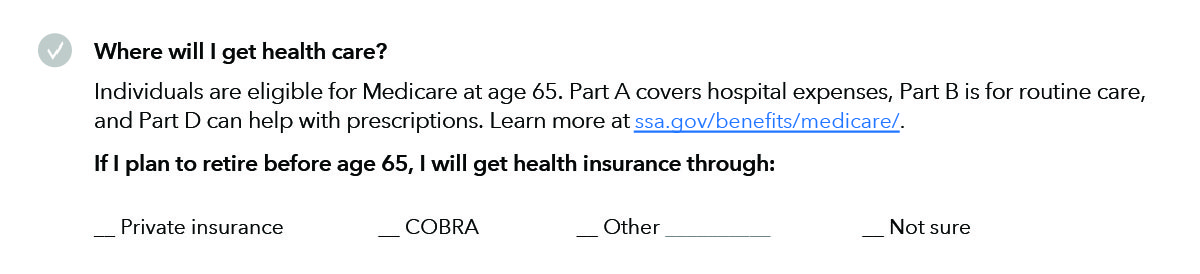

Clients often have questions about health care in retirement: Where will it come from, and what will it cost? The next questions are good reminders of some of the considerations before retirement.

Even higher net worth individuals need to understand how their current insurance benefits compare to Medicare at age 65, as well as any transitional retirement benefits through the employer or through the Consolidated Omnibus Budget Reconciliation Act (COBRA). A high-level understanding of Medicare basics is also handy when advising clients approaching age 65.

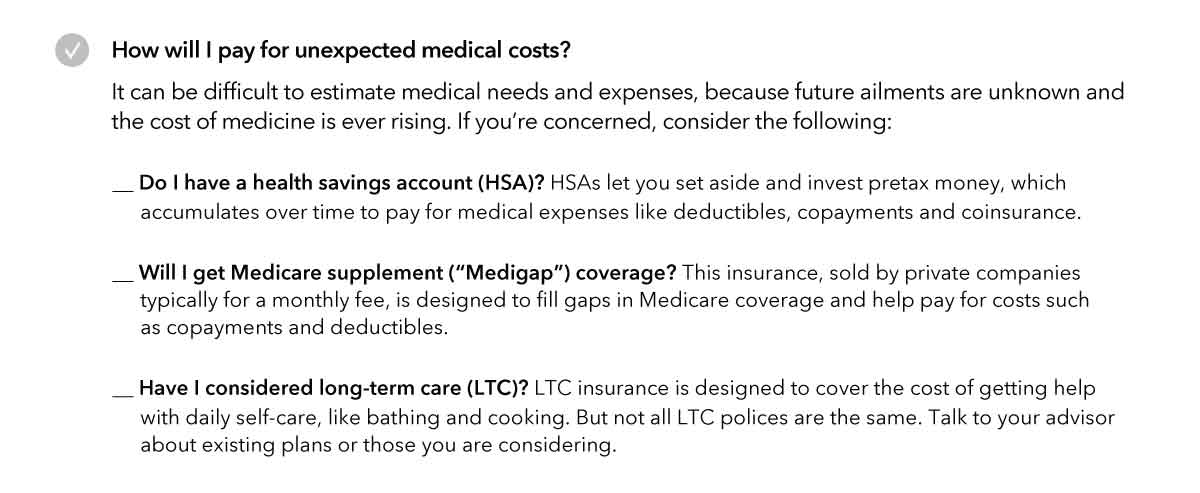

Factoring in health care costs is likely part of the retirement planning you do for clients. A few savings and insurance options are highlighted in the workbook: health savings accounts, Medicare supplement plans and long-term care insurance.

All of these plans are better approached with professional advice in mind. Be prepared to have some of these talking points at the ready.

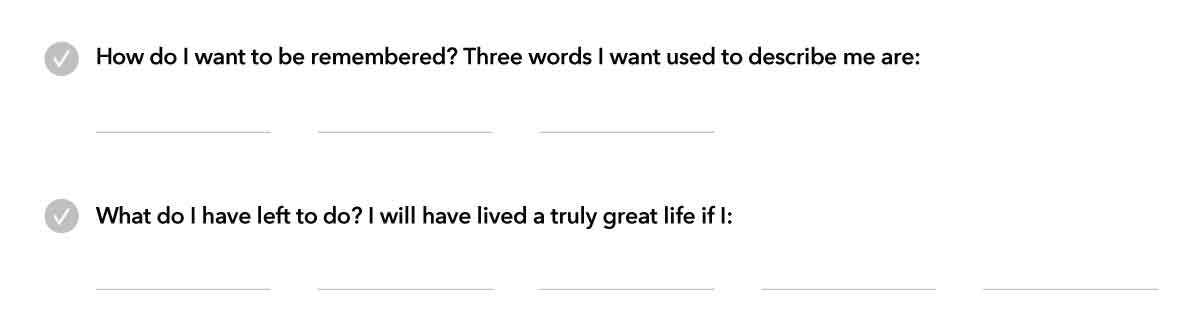

3. Values and legacy planning

This part of the plan lives somewhere between traditional retirement planning and planning for modern midlife. The idea is to define what’s important, and then find ways to support those causes through charitable and estate planning. And defining what’s important starts with a few more “big” questions about how you want to be remembered.

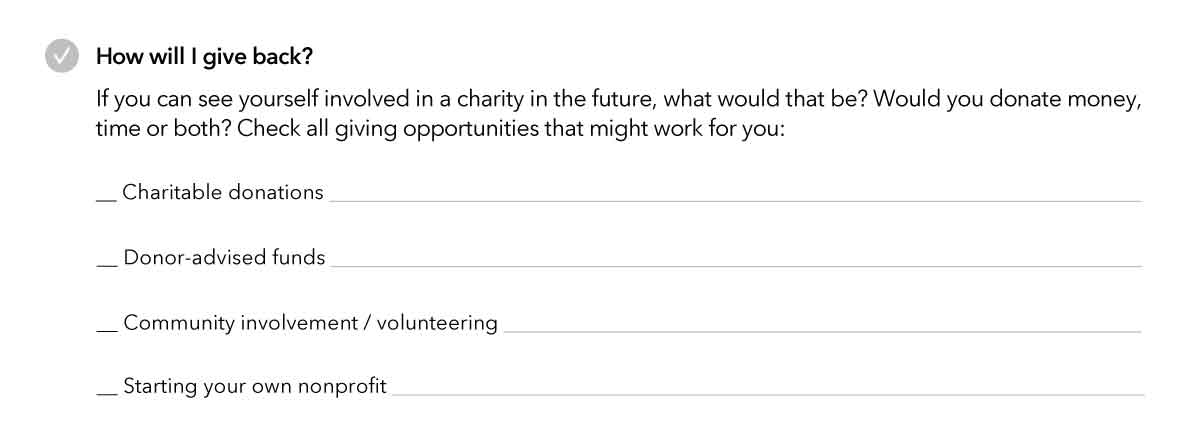

For many people, the answers lie in giving back, either through charitable giving or nonprofit work, community involvement and volunteering. Particularly among individuals who feel they have benefited from a good life, giving back can be a truly rewarding experience. With our simple list of potential opportunities, you can gauge interest in the level of planning the individual might need, where to start or where they may have questions.

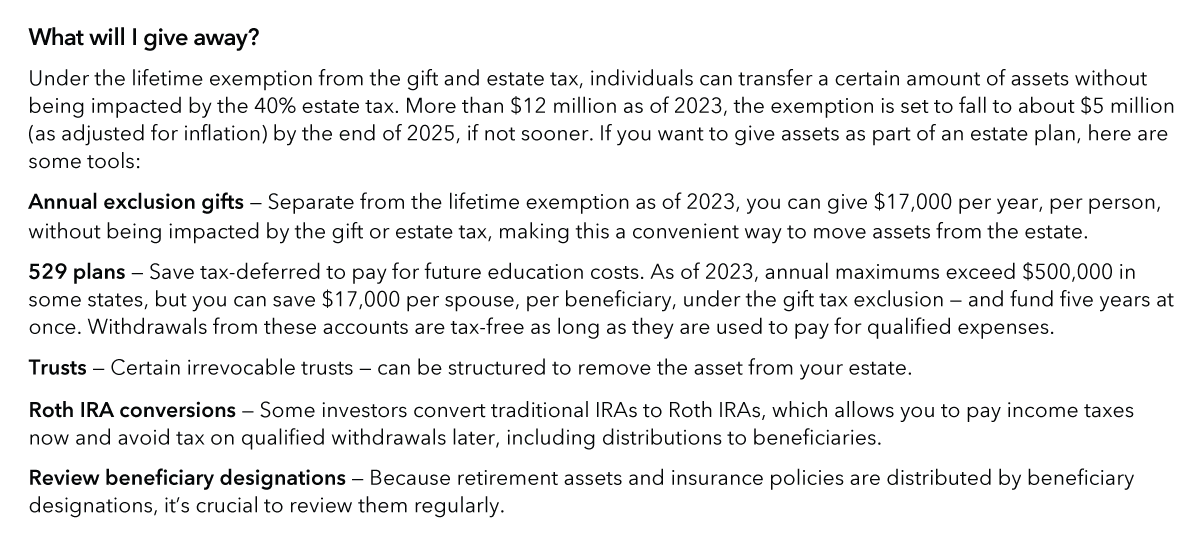

Then there are estate tax considerations. Nearly $13 million as of October 2023, the estate tax exemption is set to fall to about $5 million (as adjusted for inflation) by the end of 2025, and there is talk in Washington that it could happen sooner. This major shift could impact a great deal more of your clients in the future.

In the workbook, we offer tools individuals can use to transfer a certain amount of assets out of the estate under the lifetime exemption from the gift and estate tax.

Anyone giving away assets in an individual retirement account (IRA) should make sure beneficiaries are up to date. This has become more important under the Setting Every Community Up for Retirement Enhancement (SECURE) Act, as the stretch provisions for many inherited retirement accounts have been eliminated and replaced by the so called "10-year rule." That means instead of being able to stretch out the distribution of the account over their life expectancies, many beneficiaries will now be required to withdraw the entire account within ten years of the account owner’s death.

4. Financial planning

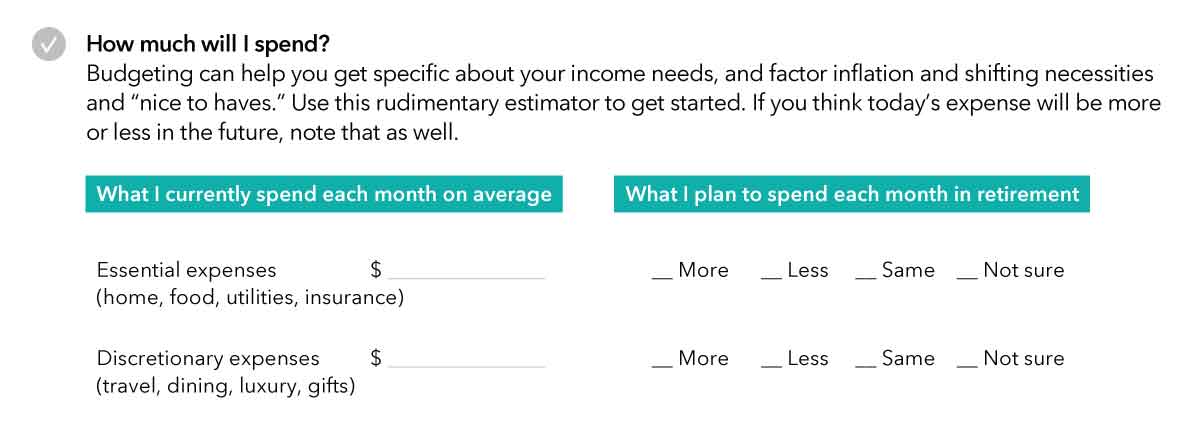

To be sure, the financial aspects of retirement are where most advisors excel. Our workbook helps bring individuals into the conversation, first by considering their spending, then listing assets and savings, and figuring where Social Security and other income fits in.

Even a very simple budget can be enlightening. Rather than listing everything you might need or spend, start by thinking of what’s spent today and try to estimate if it will be more, less or the same in the future.

To help individuals think about a portfolio withdrawal strategy — and about living without a steady employer paycheck — encourage them to pull together a full picture of their assets. As an advisor, you may not always have full access to this information that’s so crucial to building a complete plan. This is one way to start a conversation about asset consolidation.

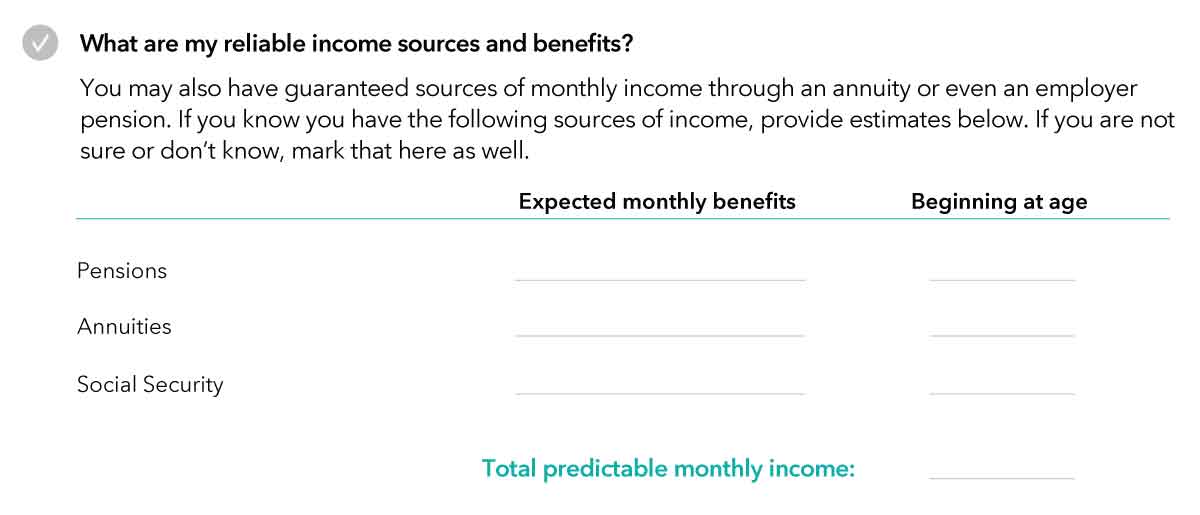

Of course, it’s also important to consider other reliable sources of income that individuals can expect to receive in retirement. Listing these can help you identify gaps in income or expectations as you plan the future of the retirement investment portfolio.

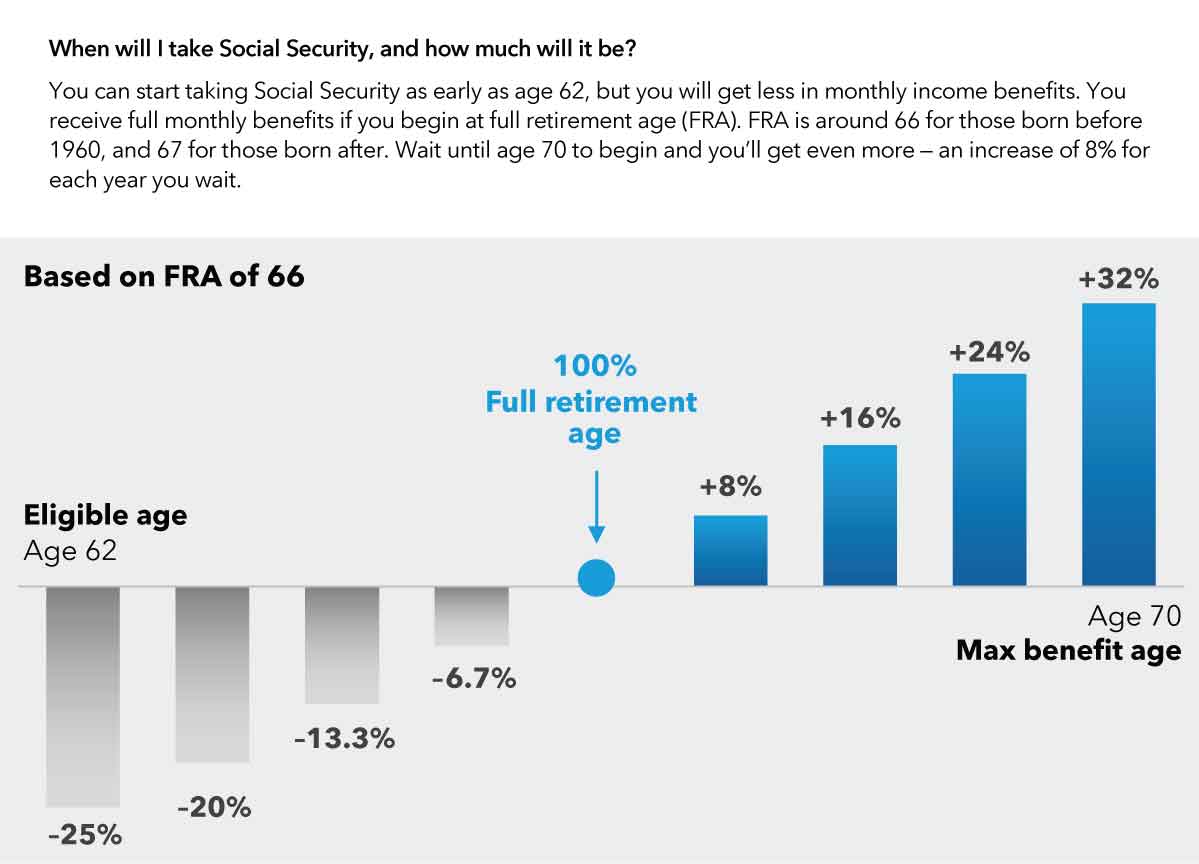

To help put all of the pieces in place, an understanding of Social Security can enhance the service you provide to clients. You can provide facts about the timing of when to begin, how divorce and remarriage factor in, how to weigh longevity versus immediate benefits, and other crucial questions investors have about Social Security.

Source: SSA.gov

Finally, remember to share this workbook with both members of a couple, and encourage them to each complete it individually and possibly together. It helps when couples enter this new phase feeling like a team. While divorce rates are currently at a 50-year low, they are rising among the over-55 set. In fact, about 43% of divorces occur in the 55+ age group, according to recent U.S. Census Bureau data as of April, 2021. A shared vision or mutual expectations for retirement may help mitigate some of this marital discord, and identifying any rifts now can only help make the plan stronger.

Related content

-

Client Relationship & Service

-

Practice Management