Retirement Planning

10 MIN ARTICLE

At Capital Group, we hear from thousands of financial professionals each year about the questions they get most from clients. Social Security is usually at or near the top of the list. Here are six essential questions your clients may have about Social Security, and how to help answer them.

TABLE OF CONTENTS

- How does Social Security work and who qualifies?

- When should I start taking Social Security benefits?

- How does marital status affect Social Security benefits?

- What if I want to keep working and get Social Security?

- How can I make the most of my Social Security benefits?

- Will Social Security be there when I retire?

For something generally thought of as ordinary and predictable, Social Security can be an exercise in frustration. For one thing, it’s an important source of income in retirement for many investors. Along with other sources, such as personal savings and retirement accounts, Social Security can help form the bedrock of an individual’s regular monthly “paycheck.”

Even for clients with higher wages, Social Security may account for about 27% of income in retirement.* Depending on longevity, the benefits could amount to more than $1 million over a recipient’s lifetime.** Or it could amount to less, depending on a few key decisions made by individuals early on in the benefits process. Understanding these decisions and their ramifications is crucial, but it’s also complicated.

As a financial professional, you can help your clients understand the importance of those decisions by navigating the complexities of Social Security and offering straightforward strategies. Meanwhile, by encouraging clients to optimize Social Security benefits, you are helping them pursue monthly income goals now and throughout retirement.

Furthermore, if you don’t offer Social Security guidance to clients, you may be at risk of losing them. Today’s investors increasingly view retirement as a complex life stage requiring holistic planning and strategic decision-making on all fronts — life planning, health and wellness, values and legacy planning — not just financial planning. Providing guidance on Social Security can help you deepen the engagement with clients in or near retirement, demonstrating your facility with important topics that go beyond the investment portfolio.

“Because each client has unique circumstances, your role of helping them understand their options for claiming Social Security to make an informed decision is crucial,” says Max McQuiston, a wealth management consultant with Capital Group. “When you spend the time to understand all the options, you’re in a position to provide better, more customized advice.”

At Capital Group, we talk to thousands of financial professionals each year, and have identified six essential questions they hear most about Social Security. Here’s how to help answer them.

1. How does Social Security work and who qualifies?

Even if you know a bit about Social Security, it helps to brush up on the basics. The program provides guaranteed lifetime income benefits that are adjusted annually to account for inflation. It is funded by taxes paid on employment income. Each U.S. worker gets a credit for a certain amount of income earned. In 2023, one credit is received for each $1,640 of earnings, up to the maximum of four credits per year. In 2024, it's one credit for each $1,730 in earnings. Anyone with at least 40 credits (around 10 years of work, full or part time) is generally eligible to receive Social Security benefits at retirement. If you worked earlier in your life and stopped, the credits you earn are still there, and future work would add to that balance.

Social Security may also provide benefits for the spouses, ex-spouses, widowed spouses and other dependents of the retired worker’s family (as well as disability benefits for workers of any age who are in need). So if you didn’t work, but a spouse or ex-spouse did, you might also be eligible for some amount of benefit. (More on this below.)

The maximum monthly benefit is $3,627 in 2023 and $3,822 in 2024, which would go to a maximum wage earner who begins taking benefits at age 70. The size of your monthly benefit will depend on how much you have earned during your working life, but it also depends on when you choose to start receiving Social Security.

Source: Social Security Administration

2. When should I start taking Social Security benefits?

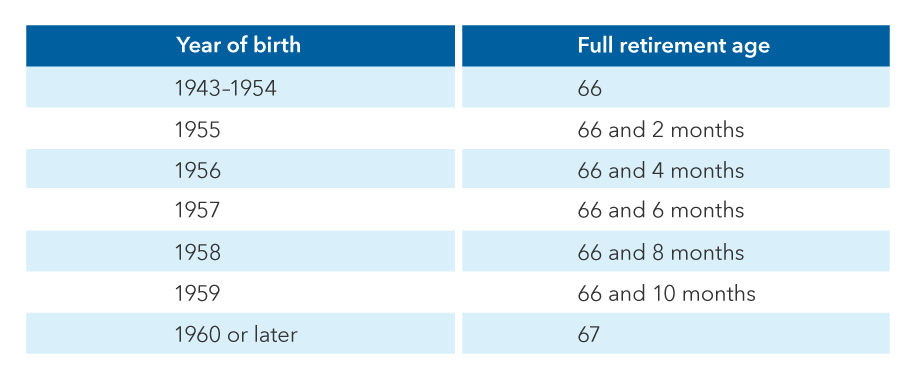

This is the biggest decision individuals have to make. Your Social Security benefit will be influenced by the age you are when you begin receiving those benefits. You may choose to begin receiving benefits as early as age 62 — earlier if you are disabled, or at age 60 if you are a widow or widower. This decision generally determines the level of monthly income you receive over your lifetime. Social Security defines the age it expects you to retire with full benefits as your full retirement age (FRA). Depending on when you were born, your FRA is currently between age 66 and 67.

Age to receive full benefits

Also known as “normal retirement age,” full retirement age may include some months as well. If you were born on January 1, refer to the previous year.

Source: SSA.gov

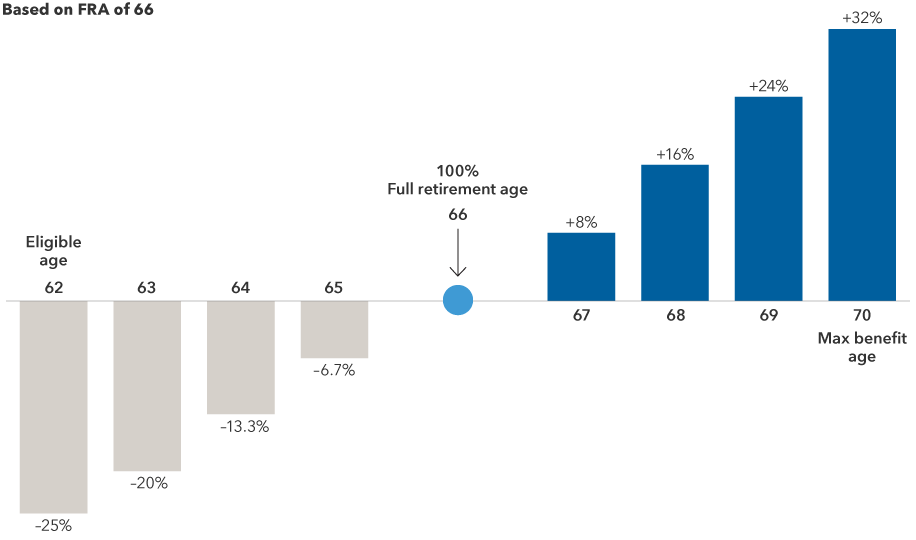

If you start receiving Social Security benefits earlier than your FRA, you get less in monthly income benefits. Starting at age 62 can reduce your monthly income by as much as 25%. If you hold off on receiving benefits until after your FRA, you can increase your monthly benefits by about 8% a year — adding as much as 32% to your benefit at FRA if you wait until age 70.

The benefits of waiting

Retiring early reduces the amount of income you receive each month. Delaying retirement increases it.

Source: SSA.gov

To understand the impact of taking benefits early, consider a hypothetical couple who are thinking of taking benefits when the husband turns 62. Based on his earnings, he can start receiving $1,200 per month now or $1,600 per month if he waits until age 66. His wife wants to work up to FRA, when she will receive a monthly benefit of $1,100.

If he starts now, by the time his wife retires, the two will have a combined monthly income of $2,300. If he waits until FRA like she does, that monthly benefit amount increases to $2,700; and if he waits until age 70, the monthly benefit adds up to more than $3,200. For some couples, this difference in steady income can be crucial to supporting their long-term needs.

On the other hand, those who start earlier can experience several months or years of accumulation of Social Security benefits. They may need the income, have health concerns or just want to get away from their jobs. Or they may simply want to enjoy years of early retirement. Depending on longevity, those who wait do not always realize greater lifetime income benefits, and in hindsight may regret not taking advantage of that valuable time.

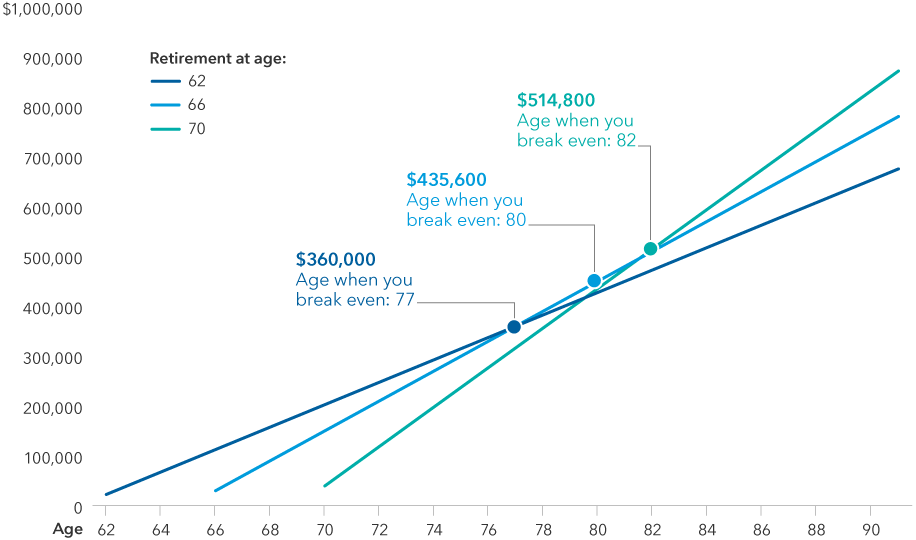

That’s why some people use their “break-even” age as part of the consideration for when to start. If you decide to wait, how long will it take for your total benefits to break even and for you to start coming out ahead? If you start at age 66, for example, you may reach age 77 before you break even compared to someone who started at age 62. Wait until age 70, and you still have to wait until age 80 to come out ahead.

Break-even analysis

While there are benefits to waiting, break-even analysis can show you how long it could take before the decision really pays off. In the below hypothetical example, see the comparison of an individual who would receive $2,500 in monthly benefits at full retirement age (age 66) compared to starting to collect benefits at 62 or starting to collect benefits at 70.

Source: SSA.gov. Does not factor in cost of living or other adjustments.

Whether a client waits or starts right away may depend on many factors: health concerns, life expectancy, reliance on the steady income stream, career plans for your 60s and 70s, and so on. This is why “When should I start?” can be more difficult to answer than it sounds.

3. How does marital status affect Social Security benefits?

Your current or past marriage may impact your benefits. Even being a parent may have an impact. Here’s how.

- Married. Marriage does not necessarily impact your Social Security benefits at retirement. If you and your spouse both have work histories, you will each collect your own benefits separately. However, if you are married and did not work or work enough to qualify on your own, you may be able to receive benefits on your spouse’s record, up to half of the amount that your spouse receives.

Or, if you both worked and qualify for benefits on your own, you can decide whether to apply for spousal benefits as well. Social Security will pay your benefits first, but if your benefits as a spouse are higher, you will get a combination that is equal to the higher benefit amount. Again, if you or your spouse take benefits prior to full retirement age, your monthly income will be reduced. But that may make sense for one spouse now who may get higher spousal benefits later. Couples can explore the impact of various options.

- Divorced. If you were married for at least 10 years but are now divorced, you generally qualify for the same spousal benefits from your ex-spouse when you reach age 62. If your individual benefits are higher, you will get yours instead.

If you remarry, you no longer qualify for benefits on your ex-spouse’s record. But if you are single at 62, you qualify whether your ex has remarried or not.

- Widowed. Widows and widowers generally qualify to receive survivor benefits beginning at age 60 (or age 50 if you are disabled). If you are widowed and remarry prior to age 60, you no longer qualify for survivor benefits. After age 60, your marital status does not affect your survivor benefits.

There are also survivor benefits for divorced individuals who have lost an ex-spouse they were married to for at least 10 years. If you are divorced and did not remarry before age 60, you may be entitled to survivor benefits.

- Parents. If you have children younger than 18, they may be eligible to receive survivor benefits through Social Security until age 18. Disabled children (those who were identified as disabled before age 22) qualify for benefits for life. If you are a widow or widower caring for a deceased worker’s child who is under 16 or disabled dependent, you are automatically eligible for benefits regardless of your age. Parents who are dependent on their adult children and are at least 62 may also qualify for survivor benefits.

4. What if I want to keep working and get Social Security?

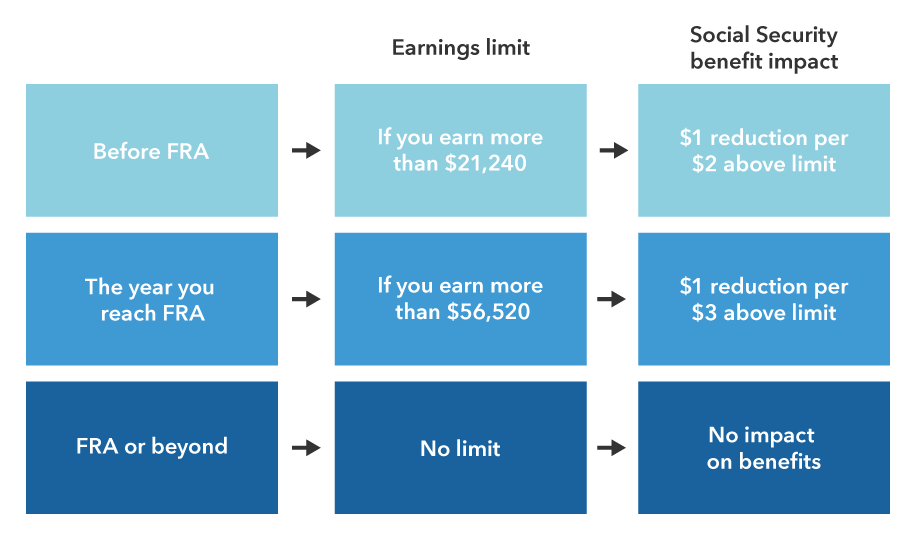

Another important timing factor is whether you want to keep working while receiving retirement benefits. You can work and receive Social Security retirement benefits, but if you are getting benefits before FRA, there’s a limit to how much you can earn before your benefits are reduced. For example, benefits are reduced by $1 for every $2 earned above $21,240 in 2023 or above $22,320 in 2024. In the year you will reach FRA, $1 in benefits is deducted for every $3 earned above a different limit, which is $56,520 in 2023 and $59,520 in 2024. Note that only your earnings up to the month before you reach your full retirement age are counted, not your earnings for the entire year.

The earnings test

Will you continue to work after you start collecting Social Security retirement benefits? If so, you may see a reduction in benefits until you reach full retirement age. Here's what that might look like based on 2023 earnings.

Source: SSA.gov, as of 9/30/2023

Once you have reached FRA, this “earnings penalty” goes away no matter how much you earn. Your benefit amount will also be recalculated to give you credit for the months that were reduced. After that, you can work all you want with no impact on your benefits. Keep in mind, however, that you may have to pay taxes on Social Security income if you have other substantial income.

5. How can I make the most of my Social Security benefits?

Because of the complexities of the system, there are opportunities to use timing and marital status to make the most of your Social Security income as well as your retirement lifestyle.

For example, there are many ways spouses can leverage the timing of their own benefits now and make changes in the future. One spouse may take benefits sooner rather than later on his or her own record, and then apply for spousal benefits in the future to increase total monthly income.

Even ex-spouses can weigh the value of taking spousal benefits compared to their own. Divorced spousal benefit is available to an ex at age 62, even if the individual has not filed on their own. As an ex-spouse, you are entitled to up to half of what your former spouse will receive at FRA. And survivor benefits for widows and widowers can be taken before or after you receive benefits as an individual.

While there is no cap or maximum on benefits received by a couple, Social Security does have a maximum family benefit that can be received on a single worker’s record. There are special formulas for computing this maximum for retirement and survival (and, in some cases, disability) benefits, which you can find on the Social Security Administration’s website.

6. Will Social Security be there when I retire?

The solvency and viability of the Social Security program may seem forever in question, and the latest annual report from the Social Security Board of Trustees states that the Old-Age and Survivors Insurance Trust Fund, which pays retirement and survivors benefits, will be able to pay current benefits only until 2033. Unfortunately, that’s a year sooner than reported in 2022. After that, the fund’s reserves and continuing tax income may pay 80% of scheduled benefits.

Clients who retire after that may expect to receive less, or there may be a change to the program before then. The report also states that lawmakers have many policy options that would reduce or eliminate the long-term financing shortfalls in Social Security and Medicare, and that addressing them sooner will help provide individuals more time to prepare for any changes.

To get more personalized Social Security answers for clients:

*Source: Social Security Administration, "Understanding the Benefits," January 2023.

**Assumption based on hypothetical individual eligible to receive $2,500 in monthly benefits at FRA, who delays until age 70 and receives $3,250 per month until age 95. Example does not factor in cost of living or other adjustments.

SUPPORTING MATERIALS

Related content

-

Retirement Planning

-

Tax & Estate Planning

-

Client Conversations