While most people know exchange-traded funds (ETFs) offer tax advantages over mutual funds, few understand how,and there’s even some confusion about whether all ETFs share the same level of tax efficiency. We break it down below.

How do ETFs offer tax advantages?

ETFs’ tax advantages stem from the unique way that they’re structured, which allows for two main sources of tax efficiency:

Externalization: ETFs trade in the secondary market, like a stock exchange, which largely insulates the fund from individual investors’ trading activity. In other words, if an ETF investor decides to sell shares of an ETF, a majority of the time, the transaction will occur in the secondary market, which does not involve any interaction with (or impact to) the fund.

In-kind redemptions: When selling activity on an exchange does result in a redemption from the fund, it is usually tax-free to remaining investors. ETFs generally satisfy redemption requests in the primary market through an in-kind delivery of securities to an intermediary (rather than cash), which means client redemptions from the fund do not generally create taxable events for remaining shareholders.

Authorized participant (AP): A broker-dealer that has a contracted opportunity with the ETF issuer to create and redeem shares in the primary market to meet market demand.

Capital gain liability: The tax on the profit of an investment that’s realized when the investor sells the investment.

Custom baskets: A feature of most ETFs that allow ETF issuers to create non-representative baskets of securities (i.e. not a pro-rata slice) that can be transacted with an AP in the primary market. This feature is particularly useful for rebalancing because it can help reduce the tax impact of investment changes within the fund.

ETF issuer: A firm that creates, manages and operates an ETF, establishing its strategy and working with regulators and exchanges to obtain permission to offer the fund.

In-kind transfers: A transaction in which the securities being exchanged are considered equal in value. For example, when APs are creating or redeeming shares for the ETF issuer in the primary market, the swapping of ETF shares for underlying securities (and vice versa) are considered in-kind transactions because the exchanged shares and securities are of equal value. These types of transactions can help reduce taxable transactions within the ETF.

Low-cost-basis stocks: Specific lots, or batches, of equity securities held within a fund that have appreciated from their purchase price and carry embedded, or unrealized, capital gains (i.e., the portion of securities that were purchased at a lower price relative to other lots of that same security within the fund).

Market maker: A firm that helps set the market price for the ETF in the secondary market and executes client demand.

Portfolio turnover rate: The percentage of the fund’s holdings that have changed within a 12-month period.

Primary market: The section of the capital market where new securities are issued. It’s also where APs work with ETF issuers to adjust the supply of ETF shares in the market, either creating new shares or redeeming excess shares.

Pro rata: Latin for “in proportion” and used to describe the allocations of securities ETF fund issuers deliver to APs in exchange for ETF shares.

Rebalancing: The practice of buying or selling fund assets to realign with the fund’s objectives and/or desired portfolio allocations. For index-based ETFs, this process generally occurs on a consistent schedule that matches the periodic rebalancing of its underlying index. For active ETFs, rebalancing may occur when portfolio managers change their investment convictions.

Secondary market: This is where most retail investors buy and sell securities. The most common examples are stock exchanges like the NYSE and NASDAQ, but trading in this market can occur across several exchanges, dark pools, direct broker and market maker trades.

Tax-loss harvesting: The practice of selling declining securities (in a taxable account) to realize the capital loss so it can be used to offset capital gains.

Tax-lot management: The practice of tracking the transaction dates, sale prices and cost basis of securities purchased at the same time (considered a “lot”) to help make strategic, tax-aware trading decisions.

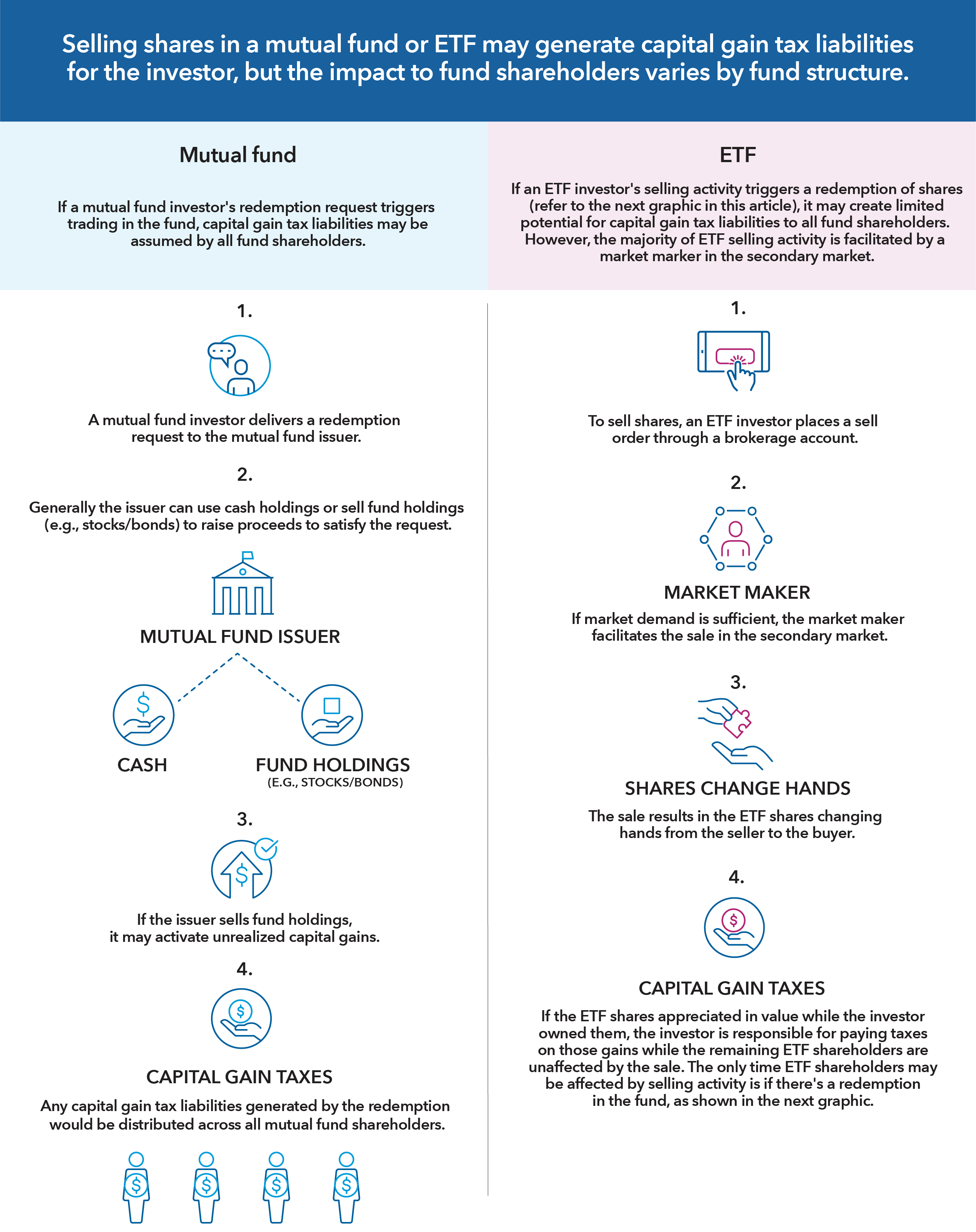

Mutual fund redemptions: A closer look

When a mutual fund issuer receives a redemption request, there are generally two ways to grant it:

Use cash held in the fund.

Sell fund holdings to raise enough cash to satisfy the request.

Fund issuers carefully consider these options with an eye toward maintaining sufficient cash holdings in the fund to meet redemption requests. If the issuer chooses to sell underlying securities, any unrealized gains crystalize, becoming capital gain distributions that impact all the mutual fund’s investors in taxable accounts. To the extent the fund has losses, it can use them to offset capital gains. (For investors in qualified accounts, reinvested distributions aren’t taxable.)

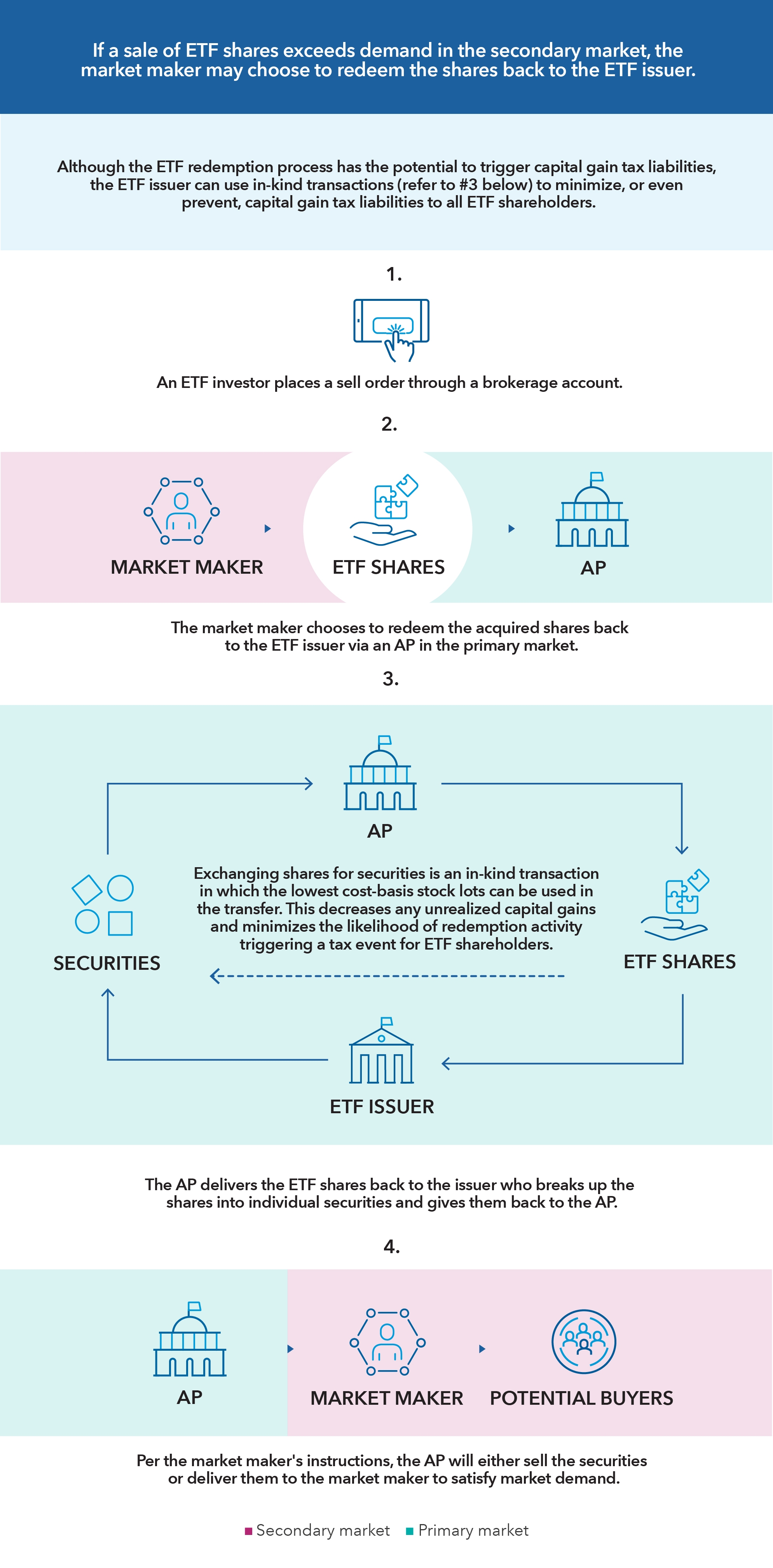

ETF redemptions: A closer look

ETF shares trade in the secondary market, such as a stock exchange, which means ETF issuers don’t need to be involved for ETF investor sales activity. The seller places a sell order through a brokerage account and executes it at a market price respective to the fund’s intraday net asset value (NAV). This execution is provided by a market maker within the secondary market. Just as an investor selling a stock may incur capital gains if the share price has appreciated since the investor bought it, individual ETF sellers will be liable for their own personal realized capital gains on any ETF shares that have grown in value since their purchase price. Because the individual ETF investor sold the shares in the secondary market, there was no impact to the underlying fund holdings. Therefore, the remaining fund holders were unaffected by the sale of shares. This can be a huge source of tax efficiency.

While most ETF transactions occur in the secondary market, occasionally, there may be a need to use the primary market. If an ETF investor sells shares in an amount that exceeds market demand, a market maker can redeem those shares in the primary market through an authorized participant (AP). APs will give back the ETF shares to the issuer in exchange for a pro-rata slice (or a representative amount) of underlying stocks held in the ETF. Because the transfer of shares for securities is in-kind, no capital gain liabilities are accrued. (However, the individual ETF investor who chose to sell shares will be responsible for any personal realized capital gains.)

Issuers of most ETFs have another tax efficiency tool at their disposal called custom in-kind negotiated baskets. This feature allows ETF issuers to create non-representative baskets of securities (i.e., not a pro-rata slice) that can be transferred to an AP in the primary market. Custom baskets can be particularly useful for rebalancing because they may help reduce the tax impact of investment changes within the fund.

These are the most basic mechanisms that allow for ETFs’ tax efficiency and, when appropriate, can be leveraged in portfolio construction tools, such as tax-lot management and tax-loss harvesting, to further enhance ETFs’ tax advantages. We’ll explore these additional sources of tax efficiency in an upcoming article.

Do ETFs distribute capital gains?

You may wonder if ETFs ever distribute capital gains, given all the tax efficiency tools at their disposal. While rare — in 2021, just 8.7% of equity ETFs paid out gains* — it’s possible, especially for ETFs that hold derivatives (which tend to be less tax efficient) and/or trade frequently, meaning they have a high turnover rate. The generally low turnover rates of passive ETFs (which aim to track the risk/return profile of an index and rebalance on the same schedule as their underlying index) may be responsible for the belief that active ETFs aren’t as tax efficient as index-based ETFs. But, as you’ll learn in the video below, active ETFs — like Capital Group’s suite of core ETFs — have the same tools at their disposal to deliver a tax-efficient outcome for investors.

How can active ETFs offer similar tax advantages as index ETFs?

In this video, Scott Davis, ETF product lead at Capital Group, examines the myth that active ETFs can’t be as tax efficient as index ETFs. He also discusses how Capital Group manages its ETFs to help investors pursue the tax advantages offered by the ETF vehicle.

For additional information about ETFs, contact your Capital Group representative.

*Source: Morningstar Direct, data as of 1/12/22 for the period ended 12/31/21.

Contact us to learn more

For more information about Capital Group’s ETFs, call our RIA support line at (800) 421-5450 or contact your relationship manager or specialist directly.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Capital Group exchange-traded funds (ETFs) are actively managed and do not seek to replicate a specific index. ETF shares are bought and sold through an exchange at the then current market price, not net asset value (NAV), and are not individually redeemed from the fund. Shares may trade at a premium or discount to their NAV when traded on an exchange. Brokerage commissions will reduce returns. There can be no guarantee that an active market for ETFs will develop or be maintained, or that the ETF's listing will continue or remain unchanged.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

On or around July 1, 2024, American Funds Distributors, Inc. will be renamed Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.