Retirement Income

Categories

Retirement Planning

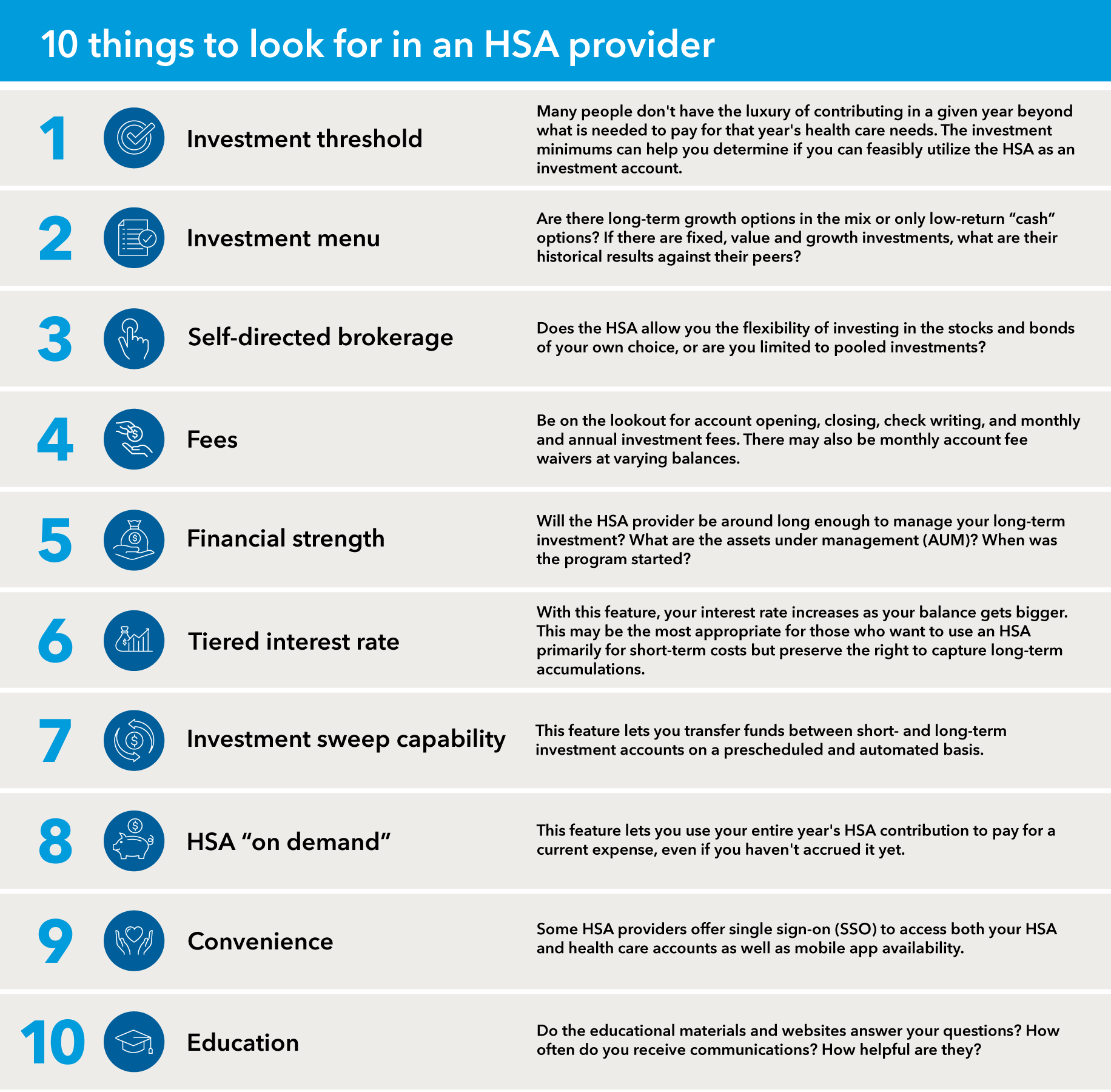

10 tips for choosing an HSA provider

Ryan Tiernan

Ryan Tiernan

November 7, 2022

KEY TAKEAWAYS

- HSAs are a great way of paying for both long- and short-term health care costs.

- Employers and employees can “decouple” their HSA from their health insurance plan provider.

- A financial professional can help you choose the HSA provider that meets your needs.

What are the two biggest savings requirements of your working years? Health care and retirement. Though employers cover both of these in benefits packages, most people view them as separate expenditures — until, that is, they reach retirement and see how much health care costs affect their retirement standard of living.

That is changing with the emergence of health savings accounts (HSAs), a unique investment strategy that can help pay for the health care–related portion of retirement spending.

Three distinct features expand HSAs from accounts that fund short-term medical expenses into long-term investment vehicles:

- Triple-tax-free benefits: Contributions are made pretax, while earnings and distributions of those earnings are tax-free for qualified health care expenses now and in the future.

- “Stow it and grow it” provisions: HSAs can be rolled over from year to year if the savings aren’t spent, unlike “use-it-or-lose-it” flexible savings accounts (FSAs).

- Individual control of account: HSAs are individual and self-directed accounts, which means you can move them to and invest them with any HSA provider, not just the one that handles your health insurance.

So how do you make the most of the HSA investment opportunity?

If you are an employee in an HSA-eligible/high-deductible health insurance plan, you can save and invest your HSA assets — the employer and employee contributions — with any provider you choose, not just the one your employer offers. This may provide greater investment opportunity, especially if your employer only offers cash-based or low-return investments from their current HSA provider.

If you are an employer, you may not know that you can expand the range of available investments by decoupling your HSA provider from your high-deductible health plan provider, who may be a health insurer that offers a less robust investment menu.

Here is a handy list of things to look for when choosing an HSA provider. Your financial professional can help you better understand and evaluate your options so you can make the best decision.

HSAs are not one-size-fits-all

HSAs were set up as a way to manage exploding health care costs. As the HSA market grows, people are starting to realize they have more choices — and more opportunity — than they may think. That’s where a financial professional can be crucial. A financial professional can help employers optimize the investment mix in their HSA based on the demographics of the business and help employees make investment decisions that may make the high cost of health care in retirement more manageable.

Learn more about

Our latest insights

This is the headline for the Newsletter promo. Customize the message.

Related Insights

-

Retirement Planning

-

Long-Term Investing

-

Never miss an insight

The Capital Ideas newsletter delivers weekly investment insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

On or around July 1, 2024, American Funds Distributors, Inc. will be renamed Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.