Retirement Income

Categories

Plan Design

What’s next for QDIAs?

Craig Duglin

Craig Duglin

January 25, 2024

KEY TAKEAWAYS

- More personalized approaches to qualified default investment alternatives, or QDIAs, are becoming higher in demand.

- Next-generation target date fund offerings may help investors better meet their needs through options that include more tailored target date funds, using a combination of multiple vintages and offering a variety of glide paths.

- Technology may make more personalized plan options easier to provide in the future; however, there are still issues to overcome.

The growth of target date funds (TDFs) has simplified retirement investing for many defined contribution (DC) participants. As qualified default investment alternatives (QDIAs), TDFs have provided many participants with more age-appropriate portfolios.

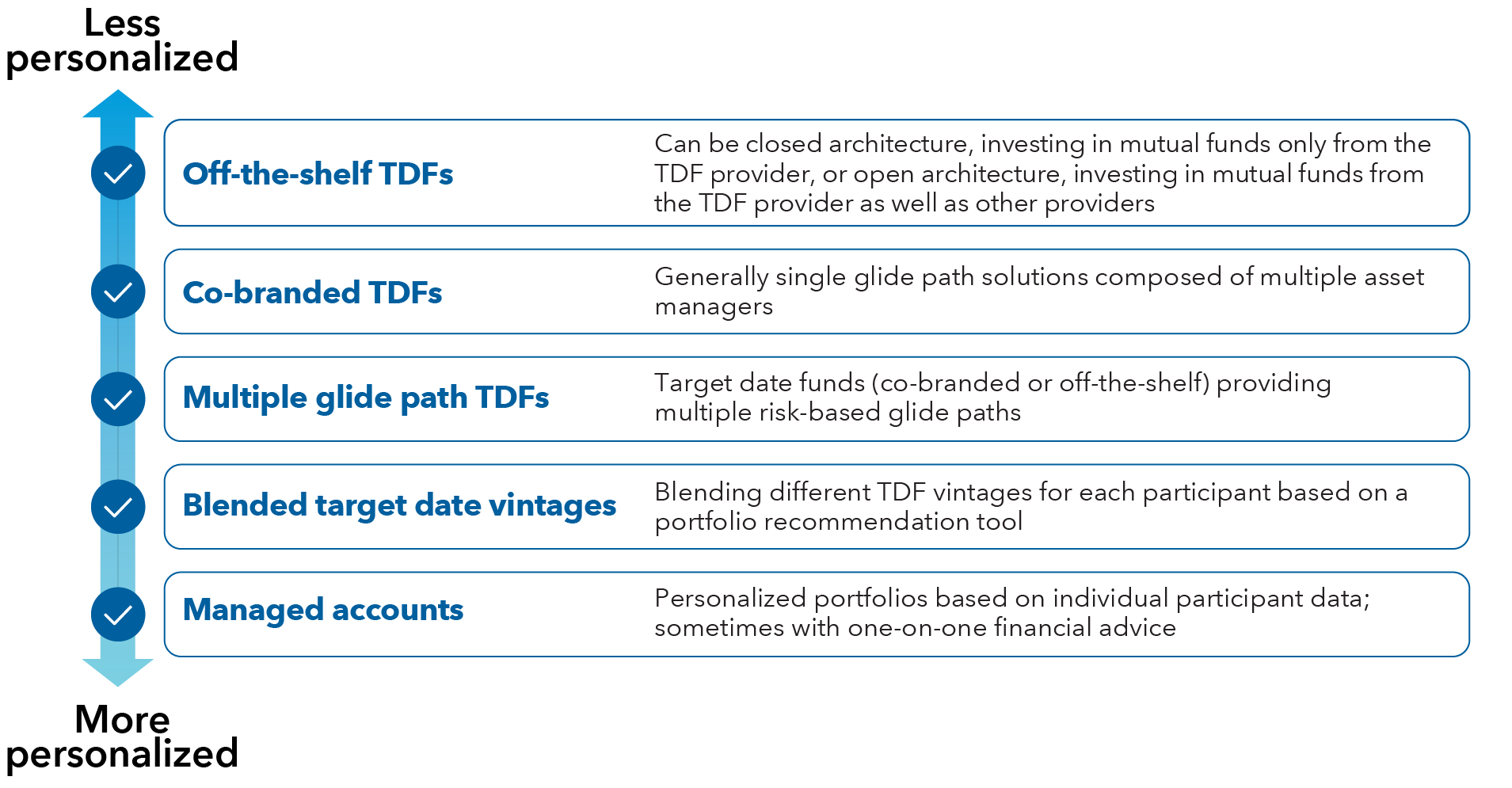

An “off-the-shelf” target date series may offer an effective solution for many participants. Yet some sponsors have found that their unique goals for the retirement plan might merit a more personalized approach.

Recordkeepers and asset managers are responding to this demand with a mix of solutions. Some are offering slightly more tailored versions of target date funds. Others are exploring QDIA solutions that provide different asset allocations based on companywide or participant-level demographic and financial data.

More tailored target date options

We are seeing some gradual shift to offering slightly more tailored versions of target date funds. For example, some target date funds are including a stable value allocation within the series. In many cases, these stable value investments are being offered in co-branded target date funds developed by asset managers and recordkeepers. These recordkeepers hire asset managers to oversee the underlying investments and may engage a third party to design the glide path. For a plan sponsor, a stable value option might be attractive because it can help manage a target date fund's volatility (unlike other fixed income investments, stable value funds are backed by insurance contracts). In addition, the inclusion of a stable value fund might allow the recordkeeper to offer more competitive fees to a plan sponsor.

Another next-generation target date option would combine different target date vintages for participants. Target date vintages are each managed toward a planned retirement year. Usually, the vintages are offered in five-year increments (a 2050 vintage, 2055 vintage, etc.) So a person retiring in the year 2046 would be defaulted into 2045 target date vintage because it is closest to her retirement date.

But a purely retirement-year approach may not work for all participants. For example, a participant planning to retire in 2035 might be willing to take on a little more risk in her target date fund. In that instance, she might want a more aggressive portfolio than a 2035 vintage.

An approach that combines multiple vintages seeks to address this problem. It would combine different target date vintages to match the participant’s risk profile or income needs. Using data provided by the participant and/or recordkeeper, an online tool could recommend that she make half of her contributions to a 2035 vintage and half to a more-aggressive 2050 vintage. Blended vintages could allow plan sponsors to offer more tailored portfolios while still using an off-the-shelf product. Although a blended system might be appealing as a default option, it requires personal and financial information provided either by the recordkeeper or the participants themselves. Because of this complexity, it may be unlikely that a plan sponsor would default participants into a blended solution.

Personalized QDIAs

Some plan sponsors are exploring more personalized QDIA solutions, including multiple glide paths and managed accounts.

Multiple glide path TDFs

Some target date providers offer employers and their participants a choice of multiple glide paths. Typically, these glide paths vary by risk and are labeled as conservative, moderate or aggressive.

Generally, a plan sponsor would choose to default their participants into the moderate glide path but could choose to default all participants into one of the other glide paths based on an analysis of employee demographics. A multiple glide path solution might be appealing to a plan sponsor with different employee demographics. For example, participants might have a mandatory retirement age of 60, or they may have access to a defined benefit plan. Depending on those factors, the plan sponsor might believe that participants would benefit from a more aggressive or conservative glide path. Alternatively, a plan sponsor could default participants into one of multiple glide paths based on their personal and financial data. However, that system likely would rely on participants to provide that data, an expectation that might not be realistic.

Managed accounts

At the full extreme of the personalization spectrum are managed accounts. Managed accounts provide each DC participant with personalized portfolios, possibly with an opportunity for one-on-one interaction with a financial professional. Typically, the managed account provider uses personal and financial data to match the participant with one of its model portfolios.

Although managed accounts are offered in many plans, they have rarely been adopted as QDIAs. As a QDIA, managed accounts offer the potential for personalization that could benefit older participants, whose financial situations are more variable than younger employees focused solely on accumulation. That’s why managed accounts are often “bolted onto” target date funds. In some cases, plan sponsors wait until participants are 50 or more years old before switching them from a target date fund into a managed account.

However, there are many issues to consider before using managed accounts as QDIAs. For example, managed accounts have overlay fees for portfolio construction, making them more costly than many off-the-shelf target date funds. Second, to be effective, managed account providers need access to participants’ personal and financial data. Ideally, the recordkeeper or plan sponsor would provide this data directly to the managed account provider. If that’s not possible, then the participants likely will have to provide that data themselves. If participants don’t provide the needed data, their portfolios may not look much different than what off-the-shelf TDFs offer – only with higher fees. For participants to fully take advantage of managed accounts, a plan sponsor needs to motivate them to engage the service – a task that may not be easy.

The future of personalization

Personalization could gain momentum for several reasons. From an implementation standpoint, technology is making managed accounts and other personalized options more affordable and widespread. Going forward, more participants may be able to enter a few data points about themselves and get a customized asset allocation recommendation. However, there are still some issues that need to be overcome, and it is important to note that the simplicity of a target date series with a single glide path and age-based gliding asset allocation is an extremely cost-effective and elegant solution for most participants.

Bear in mind that plan investment selection is a fiduciary act, and plan sponsors should apply the same due diligence to a tailored target date fund or personalized solutions as they would to any potential plan investment. They should conduct a detailed review of each provider, focusing on their costs and effectiveness. In the case of a QDIA managed account, a plan sponsor should fully consider the investment process, including the portfolio construction methodology.

Learn more about

Our latest insights

-

-

Retirement Income

-

Target Date

-

Practice Management

-

Participant Engagement

RELATED INSIGHTS

-

Retirement Income

-

Retirement Income

-

Target Date

Never miss an insight

The Capital Ideas newsletter delivers weekly investment insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Although the target date portfolios are managed for investors on a projected retirement date time frame, the allocation strategy does not guarantee that investors' retirement goals will be met.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

On or around July 1, 2024, American Funds Distributors, Inc. will be renamed Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.