Retirement Income

Categories

Practice Management

Tackling the problem of missing participants

Mike French

Mike French

November 15, 2023

Over the past decade, the problem of missing retirement plan participants — those with a balance in their former employer’s qualified retirement plan (e.g., 401(k) plans) but who have lost contact with the company — has steadily grown. As of May 2023, there are an estimated 29.2 million left behind or forgotten 401(k) accounts, with average balances of approximately $56,616.* And with a large rate of Americans leaving their jobs in the past few years, the number of such accounts has risen 20% from May 2021 to May 2023.† Yet, many plan sponsors still don’t fully understand the significance of this situation.

Rest assured, the Department of Labor (DOL) does. Their Employee Benefits Security Administration (EBSA) has stepped up audit investigations into plan sponsors who may not be doing all that they can to track down these lost participants and reconnect them with their money.

Financial professionals (FPs) have an outstanding opportunity to proactively reach out to their existing retirement plan clients and demonstrate value by shedding some light on the subject.

What causes missing participants?

In today’s transient workforce, it isn’t unusual for workers to leave a balance in their former employer’s retirement plan. But as time goes by, these workers may lose track of the plans in which they have an account, especially when events occur that change the plan (e.g., mergers, acquisitions, recordkeeper changes, changes to the plan sponsor’s name).

On the other hand, plan sponsors may lose contact with former employees when they:

- move to a new residence,

- get married or divorced and change their names, or

- pass away.

In the bustle of life changes, it may not occur to participants to contact a former employer with updated information. If the employee left involuntarily, he or she may not feel comfortable making contact.

Another type of missing participant is someone who is simply unresponsive. They may have received a distribution check but haven’t cashed it. For example, someone might feel it’s not worth cashing a $10 check for a trailing dividend that was credited to their account.

And in some cases, former employees (such as those who were auto-enrolled in the plan) may not even realize they have an account at all. So, they never seek to claim what’s rightfully theirs.

FPs can emphasize to clients that the longer a participant goes missing, the harder it can be to find them later. Some early red flags to watch for may include distribution checks, quarterly statements or service emails that are sent but returned undeliverable.

What’s at stake

A missing participant can be a costly proposition for participants and plan sponsors alike.

Participant: In the face of a serious nationwide retirement savings gap, many investors can’t afford to leave money on the table that could otherwise help them retire with dignity. And in the event of their death, their loved ones could miss out on valuable beneficiary death benefits.

Some plan designs provide for the transfer of uncashed checks for missing participants to the plan’s forfeiture account after reasonable steps have been taken to locate the participant. Although the plan would be required to pay the benefit should the participant make a claim for the forfeited amount, the participant can end up worse off by missing out on any gains that might have accrued if the money had remained in the investment account.

Plan sponsors: Administrative burdens and increased plan costs aside, there is the concerning possibility that an audit may find the sponsor did not make reasonable efforts to locate missing participants and is in breach of their fiduciary duty.

Encourage clients to develop a plan of action

In their capacity as fiduciaries, plan sponsors are tasked with determining and taking appropriate steps to locate and distribute retirement benefits to missing participants. While this may seem like a daunting task, the good news is that technology and new guidance have made it easier than ever for sponsors to succeed.

FPs serving these clients can offer ideas to consider:

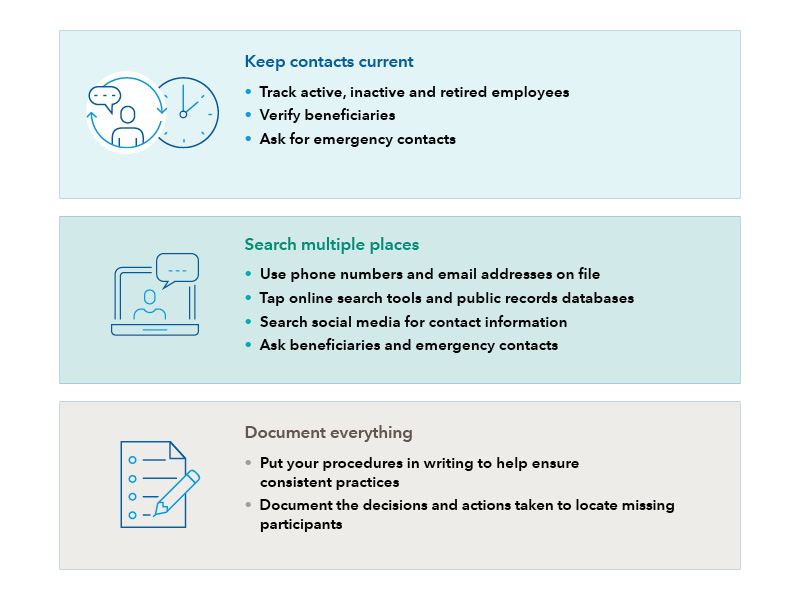

- Decide who will manage missing participants — Guidance from the DOL (see below) states “the first step in addressing any problem often is knowing that there is one.” Many plan sponsors believe that their plan’s third-party administrator (TPA) and/or recordkeeper are responsible for locating missing participants. But unless these providers have agreed to provide such a service, the plan sponsor is responsible. Therefore, the plan sponsor should ask service providers about their policies and procedures relating to locating missing participants.

Many recordkeepers can provide a report of participants with uncashed checks and undeliverable mail and/or email. That can serve as a starting point for managing lost participants.

Plan sponsors may want to consider delegating the responsibility to a third-party service provider that specializes in this area. It is important to remember that while sponsors may delegate to third-party service providers, it is their fiduciary duty to ensure that the delegate’s procedures are adequate.

- Formalize a plan – If the plan sponsor retains the responsibility for managing missing participants, they will need to determine the steps they will take to locate missing participants. Any processes or procedures that are implemented should be documented and followed. Having sufficient documentation could be especially important in the case of a DOL audit.

To help plan sponsors understand their obligations regarding missing participants, in January 2021 the DOL issued “best practices” guidance for maintaining participant information and locating lost participants and beneficiaries. This guidance details steps that plan fiduciaries should consider to locate and distribute retirement benefits to missing or nonresponsive participants.

While Missing Participants — Best Practices for Pension Plans does provide some helpful insight, it falls short of creating any type of “safe harbor” for plan fiduciaries to rely upon. It does, however, allow a plan sponsor to consider what search measures might be appropriate for its particular plan, including balancing the size of the account involved against the cost of the search efforts.

Examples of best practices from the DOL

Congress acts

The issue of missing participants has been such a problem that the SECURE 2.0 Act of 2022, passed in December 2022, includes provisions aimed at helping participants locate their benefits held in former plans and minimizing the number of missing participants:

- Auto-portability: Certain small retirement plan account balances for terminated employees can be automatically rolled into a default individual retirement account (IRA). Employer plans will have the option of automatically transferring a participant’s default IRA from a previous employer into the participant’s current employer plan unless directed otherwise by the participant. Among other things, this may help reduce the number of future missing participants due to accounts being held in prior employer plans.

- Retirement savings lost and found: To help individuals find information about previous employers to claim earned benefits, the DOL will create a searchable retirement savings database. The database will enable individuals, who might have lost track of their retirement plan, to search for the contact information of their plan administrator.

Learn more about

* Source: Capitalize, “The True Cost of Forgotten 401(k) Accounts (2023).”

† Ibid.

Our latest insights

-

-

Retirement Income

-

Target Date

-

Practice Management

-

Participant Engagement

RELATED INSIGHTS

-

Retirement Income

-

Retirement Income

-

Target Date

Never miss an insight

The Capital Ideas newsletter delivers weekly investment insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

On or around July 1, 2024, American Funds Distributors, Inc. will be renamed Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.