Retirement Income

Categories

Regulation & Legislation

6 things every advisor should know about the SECURE Act

Jason Bortz

Jason Bortz

Jeffrey Brooks

Jeffrey Brooks

Leslie Geller

Leslie Geller

January 22, 2020

A new year brings with it sweeping new federal rules affecting U.S. retirement plans.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act is the most significant retirement-related legislation in more than a decade. Among many provisions, the law allows savers to delay required distributions, make penalty-free withdrawals for certain expenses and offers new tax incentives for small-business retirement plans.

Here’s an overview of some of the key measures taking effect in 2020:

1. Savers can wait until age 72 to take required minimum distributions

The new age threshold applies to individuals who reach age 70½ in 2020 or later. Those who turned 70½ in 2019 will not be able to take advantage of the new law and will still need to take required distributions on the previous timeline.

Notably, the age threshold for making qualified charitable distributions (QCD) from an IRA remains at 70½. This means there’s a one- to two-year period during which an individual does not have to take distributions from their IRA but can still make QCDs on a pre-tax basis.

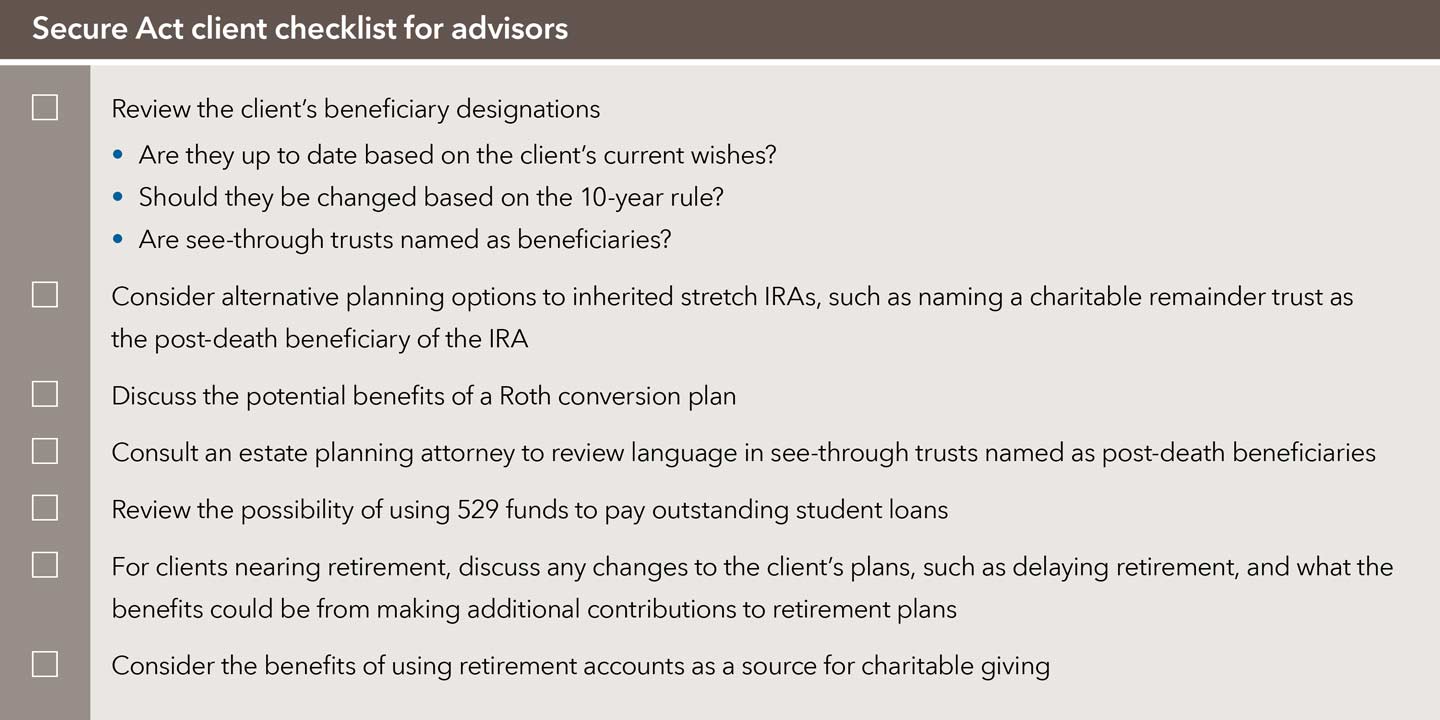

2. Keep an eye on the 10-year rule for stretch IRAs

The stretch provisions for many inherited retirement accounts have been eliminated and replaced by the 10-year distribution rule. That means beneficiaries who inherit retirement accounts in 2020 or later, instead of being able to stretch out the distribution of the account over their life expectancies, must have the entire account disbursed to them by the end of the 10th year following the year of inheritance. Along with this acceleration of distributions comes an acceleration of the income taxes with respect to these distributions. However, because there are no additional distribution requirements within that 10-year period, beneficiaries may have some new opportunities to optimize tax efficiency, given the flexibility to time distributions (or defer them entirely) during the 10-year period.

Certain beneficiaries are excluded from the 10-year rule and can still abide by the old lifetime stretch rules, including a surviving spouse, a child of the original account owner who has not reached the age of majority (but only until they reach the age of majority), a beneficiary that is less than 10 years younger than the deceased account holder, and chronically ill or disabled beneficiaries. If instead of an individual a trust is named as the beneficiary of an inherited retirement account, the trust should be reviewed by an estate plan attorney. Specially designed trusts often referred to as see-through trusts were likely drafted in accordance with the old lifetime stretch provisions, and the application of the new legislation could result in inconsistencies and unintended consequences.

3. Contribute to a traditional IRA past the age of 70½

Contributions to traditional IRAs by those aged 70½ or older are now permitted as long as employment income is still coming in. (Contributions to Roth IRAs post age 70½ have always been permitted and will continue to be so.) Keep in mind, post-age 70½ contributions to traditional IRAs may affect an individual’s ability to make QCDs. Starting at age 70½, individuals can annually make up to $100,000 of QCDs, which allow IRA funds to be used for certain charitable contributions on a pre-tax basis. However, the act does add language that prevents an individual from distributing as QCDs any deductible contributions made to traditional IRAs for the year that the individual reaches age 70½ and for years thereafter.

4. Make penalty-free withdrawals to help with the birth or adoption of a child

New parents may take $5,000 per person in penalty-free withdrawals from retirement accounts to help with birth- or adoption-related expenses. That means a couple can withdraw $10,000 per child. The withdrawal must be made during the one-year period following the birth or finalized adoption date of a child. The withdrawals are included in taxable income. The amount may be repaid at a later time as an additional contribution to a parent’s retirement account, which can be over and above an individual’s standard contribution limits.

The requirements around the timing of these repayments and their tax consequences are still a bit unclear. Further clarification is likely to come from future regulations by the U.S. Treasury Department.

5. Take a look at the new incentives for small-business retirement plans

Small businesses starting their first-ever retirement plans have been eligible to receive a federal tax credit to offset 50% of the expenses incurred by the employer in connection with the plan. That tax credit can be used for up to three years after the plan’s launch. The SECURE Act significantly increases the tax credit from a maximum of $500 a year to $250 for each non-highly compensated employee who is eligible to participate in the plan, up to $5,000 a year. The credit is available for SIMPLEs, SEPs and 401(k) plans.

6. Be aware of expanded eligible expenses for 529 accounts

529 plans may now be used to pay for certain student loan expenses up to a $10,000 lifetime maximum as well as certain apprenticeship program expenses. The act makes these changes retroactive to distributions made after December 31, 2018.

In addition to using 529 funds to pay the account beneficiary’s student loan debt, up to $10,000 can be used to pay down the student loan debt of each of the beneficiary’s siblings. Keep in mind, if withdrawals are used for purposes other than qualified education expenses, the earnings will be subject to a 10% federal tax penalty in addition to federal and, if applicable, state income tax.

A potential benefit of this new provision is that grandparents who want to help pay for college can do so to a certain degree without affecting the student’s financial aid eligibility. So, instead of paying tuition directly from a 529 funded by a grandparent, which can affect financial aid eligibility, the grandparent can wait and use the funds to help repay the student’s loans.

Learn more about

Our latest insights

This is the headline for the Newsletter promo. Customize the message.

Related Insights

Never miss an insight

The Capital Ideas newsletter delivers weekly investment insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

On or around July 1, 2024, American Funds Distributors, Inc. will be renamed Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.